This guide compares federal MSB requirements with state MTL obligations, when you need each, and your compliance pathway.

Quick Comparison: MSB vs MTL

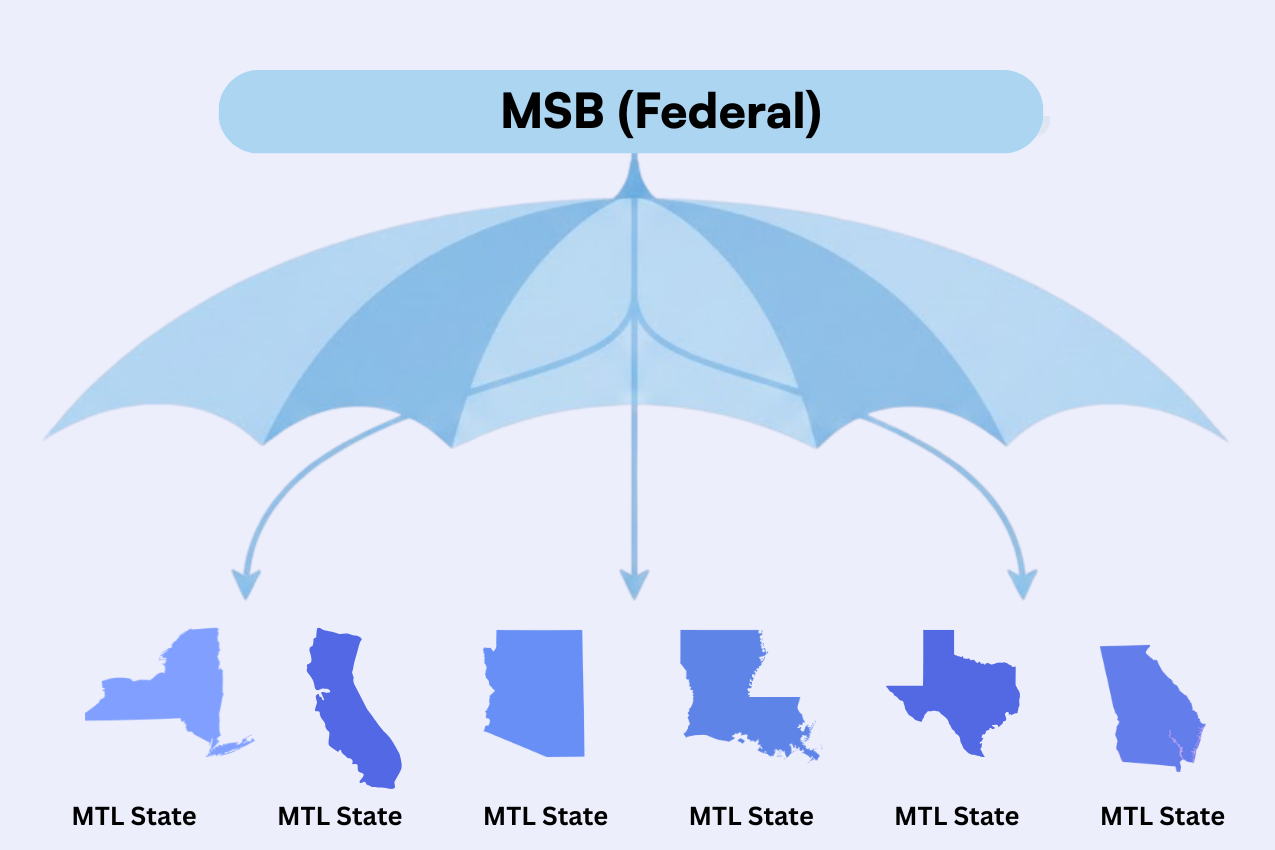

Here's the short version: MSB (Money Services Business) is a federal classification, while MTL (Money Transmitter License) is a state-issued license. All money transmitters are MSBs, but not all MSBs are money transmitters. The relationship is hierarchical: think of MSB as the umbrella category and MTL as one specific type of license within that category.

MSB (Money Services Business) = Federal FinCEN registration for non-bank financial services.

MTL (Money Transmitter License) = State authorization for receiving/transmitting funds. See What is a Money Transmitter License.

| Aspect | MSB (Federal) | MTL (State) |

|---|---|---|

| Authority | FinCEN | 49 states + D.C. |

| Cost | $0 | $250K+ Year 1 |

| Timeline | 2-6 weeks | 3-18+ months |

| Net Worth | None | $100K-2M |

| Threshold | >$1K/day (except transmitters) | Any volume triggers |

| When Needed | All 6 MSB types | Money transmitters only |

Regulatory Authority: Federal vs State

Understanding the relationship between federal and state regulatory frameworks is essential for building a compliant operation.

Regulatory Authority

MSB registration falls under federal jurisdiction. FinCEN, part of the U.S. Treasury Department, oversees MSB registration and enforcement of federal AML requirements. The IRS serves as FinCEN's delegated examiner for BSA compliance.

MTL licensing is handled at the state level. Each state has its own banking regulator—the Department of Financial Services in New York, the Department of Financial Protection and Innovation in California, and so on. These state regulators issue licenses, conduct examinations, and enforce state money transmission laws.

Scope and Purpose

The MSB classification is primarily designed for anti-money laundering purposes. Federal regulators want to ensure that non-bank financial institutions implement appropriate controls to detect and prevent money laundering and terrorist financing. MSB registration brings companies into the BSA regulatory framework, requiring AML programs, suspicious activity reporting, and currency transaction reporting.

MTL licensing focuses on consumer protection and prudential oversight. State regulators want assurance that money transmitters are financially stable (hence net worth and surety bond requirements), operationally sound, and capable of fulfilling their obligations to customers. State examinations review both AML compliance and broader operational controls.

Registration vs Licensing

MSB registration with FinCEN is relatively straightforward. Companies complete FinCEN Form 107 electronically, provide basic business information, and renew registration every two years. There's no application fee for federal MSB registration, and approval is typically quick.

MTL licensing is substantially more involved. Each state has its own application process, fees, documentation requirements, and review timeline. Applications often take 3-18 months to process, require extensive documentation (financial statements, business plans, compliance policies, background checks), and involve significant costs.

Compliance Obligations

Federal MSB requirements include registering with FinCEN within 180 days of establishing the business, implementing a written AML program, filing Currency Transaction Reports (CTRs) for cash transactions over $10,000, filing Suspicious Activity Reports (SARs) for suspicious transactions of $2,000 or more, maintaining transaction records, and renewing registration every two years.

State MTL requirements vary but typically include annual license renewals with associated fees, quarterly and annual reporting (often through NMLS Call Reports), maintaining minimum net worth, keeping surety bonds current, undergoing periodic examinations, and reporting material changes (new products, ownership changes, key personnel).

MSB vs MTL: Side-by-Side Comparison

Understanding federal MSB registration and state money transmitter licensing

| Requirement | MSB (Money Services Business) | MTL (Money Transmitter License) |

|---|---|---|

| Basic Definition | Federal classification for non-bank financial services providers | State-issued license to conduct money transmission |

| Regulatory Authority | FinCEN (U.S. Treasury Department) | Individual state banking regulators (e.g., NY DFS, CA DFPI) |

| Geographic Scope | Nationwide (one registration covers all U.S. operations) | State-by-state (separate license required per jurisdiction) |

| Primary Purpose | Anti-money laundering (AML) compliance and oversight | Consumer protection and prudential supervision |

| Number of Filings | 1 federal registration | ~50 separate state licenses for nationwide coverage |

| Application Complexity | Straightforward online form (FinCEN Form 107) | Extensive documentation, background checks, business plans |

| Application Fee | No fee | $100 – $10,000+ per state (~$115K total for all states) |

| Approval Timeline | Typically 2–6 weeks | 3–24+ months per state |

| Renewal Frequency | Every 2 years | Annually (in most states) |

| Net Worth Requirement | None | $100K – $2M+ depending on state |

| Surety Bond | Not required | $10K – $1M+ per state |

| AML Program Required | Yes (federal BSA requirement) | Yes (states also examine AML compliance) |

| Reporting Requirements | CTRs, SARs, recordkeeping | Quarterly/annual call reports, state-specific filings |

| Examinations | IRS (as FinCEN delegate); limited frequency | Regular state examinations; often coordinated multi-state |

| Applies to Crypto | Yes (virtual currency exchangers/administrators) | Yes in most states (plus NY BitLicense for crypto) |

Compliance Burden: Registration vs 50-State Licensing

For money transmitters you’ll need both a MSB and MTL(s). The typical compliance pathway looks like this:

Step 1: Register as an MSB with FinCEN.

This is your federal foundation. Complete Form 107, implement your AML program, and establish your BSA compliance infrastructure.

Step 2: Apply for MTLs in your target states.

Determine which states you need based on where your customers are located, then begin the state licensing process. Many companies prioritize states based on customer concentration, strategic importance, or application timeline.

Step 3: Maintain both federal and state compliance.

Renew your FinCEN registration every two years, renew state licenses annually, file required reports at both levels, and stay current on regulatory changes.

The CSBS has worked to modernize and harmonize state licensing through the Money Transmission Modernization Act (MTMA). To date (Dec 2025), 42 states + D.C. have adopted the MTMA in full or in part. According to CSBS, money transmitters licensed in at least one state that has adopted the MTMA collectively account for 99% of reported money transmission activity. This standardization has created more consistent requirements for net worth, surety bonds, and permissible investments across participating states.

Common Misconceptions

"I only need one or the other." Wrong. If you're a money transmitter, you need federal MSB registration AND state MTLs. These aren't alternatives; they're complementary requirements at different regulatory levels.

"MSB registration is a license." Not quite. MSB registration is exactly that: a registration. It notifies federal regulators that you exist and brings you into the BSA framework. It doesn't authorize you to conduct money transmission. That authorization comes from state licenses.

"Once I'm licensed in one state, I can operate everywhere." Unfortunately, no. Each state is an independent jurisdiction. A New York license doesn't help you in California, and vice versa. The NMLS makes managing multiple licenses easier, but you still need separate approval from each state.

"Federal registration covers my AML obligations, so states don't care about AML." States absolutely care about AML compliance. While FinCEN sets federal standards, state examiners also review AML programs during their examinations. As CSBS notes, given the limited examination resources of FinCEN and the IRS, states are effectively frontline supervisors of federal AML compliance for money transmitters.

Crypto: MSB + MTL + BitLicense Layers

The MSB vs MTL framework applies to cryptocurrency businesses as well. According to FinCEN guidance, virtual currency exchangers and administrators generally qualify as money transmitters and therefore MSBs. This means crypto exchanges, wallet providers, and similar businesses face the same dual compliance requirements: federal MSB registration plus state MTLs.

New York, Louisiana (and soon California) adds an additional layer with its BitLicense requirement for virtual currency business activity. Other states have varying approaches to crypto regulation, with some explicitly including virtual currency in their money transmission definitions.

How Brico Simplifies MSB and MTL Compliance

Navigating both federal and state requirements across 50+ jurisdictions creates significant operational complexity. Brico's compliance automation platform addresses this challenge by centralizing license management, deadline tracking, and regulatory monitoring in a single interface.

Unified license tracking. Whether you're managing federal MSB registration or state MTLs across dozens of jurisdictions, Brico provides visibility into every license, renewal date, and compliance requirement from one dashboard.

Automated deadline management. With renewal dates, reporting deadlines, and filing requirements varying by jurisdiction, it's easy for something to slip through the cracks. Brico sends proactive alerts and tracks all upcoming obligations, ensuring nothing is missed during staff transitions or busy periods.

Regulatory intelligence. State requirements change frequently—new forms, updated fee schedules, revised application requirements. Brico monitors regulatory changes across all jurisdictions and surfaces updates relevant to your licenses.

Streamlined applications. Smart data mapping pre-fills application forms using information you've already provided, reducing repetitive data entry and the errors that come with it.

Ready to discuss your licensing roadmap? Contact Brico to explore how MTL licensing software can help you navigate the process efficiently.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or regulatory advice. Brico is not a law firm and does not provide legal counsel. Licensing requirements vary by state and depend on your specific business model and circumstances. You should consult with qualified legal counsel before making any licensing decisions or taking action based on this content.